| Individual Retirement Accounts (IRAs) are a nice way to save for retirement. You may be eligible to contribute to an IRA if you have ‘taxable compensation’. If you file a joint return, you and your spouse can each contribute to an IRA even if only one of you has ‘taxable compensation’. ‘Taxable compensation includes wages, salaries, commissions, tips, bonuses, or net income from self-employment. Contribution Limits for 2024 and 2025 remain the same: You may contribute up to a maximum of $7,000 ($8,000 if you are age 50 or older) to a traditional or Roth IRA annually.

Traditional IRAs may provide an upfront tax deduction and grow tax deferred over your lifetime. These contributions are subject to the Required Minimum Distribution (RMD) rules.

Roth IRAs provide no upfront tax deduction but grow tax free over your lifetime. These contributions are subject to the Required Minimum Distribution (RMD) rules.

If you currently have an IRA, or are considering opening one soon, it’s important to be aware of the year-end rules that apply to the type of IRA to which you contribute.

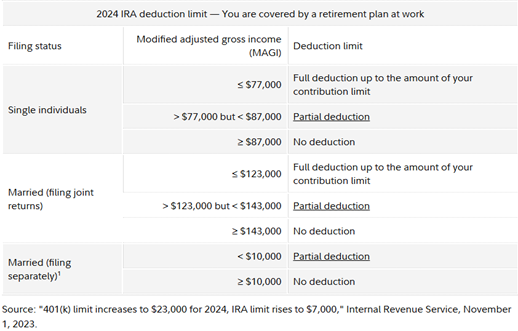

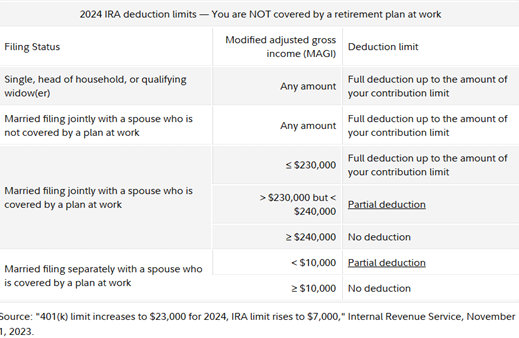

- For traditional IRA contributions, your deduction may be limited if either taxpayer or spouse is covered by a retirement plan at work. If both taxpayer and spouse are not covered by a retirement plan at work, there are not income thresholds to consider for the deduction.

- Roth IRA contributions are subject to income thresholds regardless of whether or not you are covered by a retirement plan at work.

- The deadline for 2024 IRA contributions is April 15, 2025 (and April 15, 2026 for 2025)

The 2024 income/deduction limits for Traditional IRAs are as follows: |